A Public Finance Initiative we Could Support

Molly Scott Cato

T

he economy has in recent years been displaying growing evidence of a problem of split personality. In the private sector — the arena of profit-making production and personal consumption — we see expansion and boom with gadgets and fashion-following beyond the dreams of our grandparents. Yet simultaneously our basic services and the infrastructure we all rely on — that none of us would fund individually — is breaking down. Our post office is, we are reliably informed, going bankrupt; our telecommunications system is likely to be outstripped by that of India; our trains are outclassed by those of the countries of Central and Eastern Europe.And in spite of the evidence of the need for massive public investment to ensure a quality of daily life appropriate to the world’s fourth largest economy, government cannot find enough money to invest. Why is this disparity increasing? Have we grown meaner with our willingness to pay taxes? Is there a level of tax which we could be convinced to pay that would generate enough cash to solve these problems?

I am drawing a distinction between the private and public sectors because that seems to be the line between which these disparities of investment cash occur. The reason may be made clear from the diagram. The flows between the two sectors teach us two important lessons. First, that the only way within the existing policy-making paradigm that the government can find money to invest in the public sector is by extracting it from the private sector by taxation (or by borrowing it). Secondly, while the infrastructure of this country is classed as belonging to the public sector, it is routinely used without charge by all the private businesses of this country, and without it they would be completely unable to function. A classic example of the free-rider problem so beloved of conventional economists, although none of them seem to have spotted it.

Of course this figure is far too simplistic; it is being used to make a point, but also to draw attention to the need to keep clear the distinction between these two sectors, because the political difference is crucial and is currently being blurred. This is precisely what PFI is for, so that we are no longer sure who is responsible for our public services, or who is paying for them and how. Let's take the example of Railtrack. Apparently rail services have been ‘privatised’ yet Railtrack is not, was not and never could be a private company. It is using our, publicly funded infrastructure and whatever financial messes it gets itself into we will always have to bail it out. The alternative would be to exist without a rail system, which is a political impossibility. Of course there is one way in which Railtrack is like a private company — the most important one to its shareholders — that it can make a profit.

There is an increasing number of pieces of evidence of what old-fashioned economists would call a ‘deficiency of effective demand’ in the public sector. The difference between effective demand and simple demand is the difference between what people need and what they can afford to pay for. No one would argue that people are not demanding more from the public sector: whether it is firefighters calling for professional levels of pay or local authorities strapped for cash to build hospitals or schools. Yet, we are told with tedious frequency, we cannot have these necessary services because there isn’t the money to pay for them. There is, however, money to pay for two foreign holidays year, or for complete redecoration of homes following a whim of fashion, or for exotic foodstuffs from around the world on a daily basis, and so on.

During the past ten years or so the politicians think they have solved this problem with a policy sleight-of-hand known as the Public Finance Initiative. Recognising the abundance of money in the private sector, they have decided to work in ‘partnership’ with its managers to move enough money from the sunburst to the heart to rebuild our infrastructure. The problem is that they are doing this at massive rates of interest, ensuring that the public supply of cash for future investment will be for ever indebted to the investment they make today. The only reason this has any political credibility at all is that it is accompanied by the sort off-balance-sheet accounting that did for Enron.

I can almost hear the monetary reformers screaming ‘Get to the point’,

because the point is obvious by now. Why is there an inadequate stock of money

in the public sector? — Because the public sector is no longer creating

sufficient money for its needs. Why is there superfluous cash in the private

sector forcing us to tireless consumption? — Because banks are creating money

without any government restraint and begging us to borrow more into existence

with a daily bombardment of junk mail.

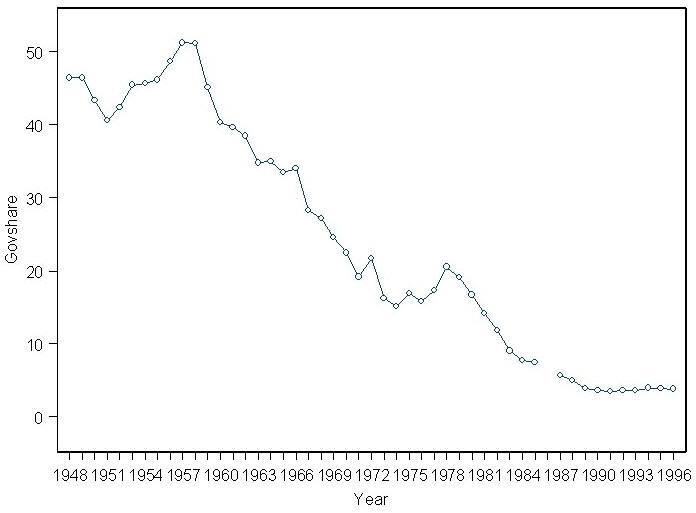

The graph shows the decline in the proportion of money created by government, instead of by private banks. This proportion has fallen from around 50% in 1948 to 30% in 1966, with a much more rapid fall in the late 1960s to a mere 16% by 1976. In 1996, the last year for which data from this source are available, the percentage created by government was around 4%; it has since fallen to 3%. (All figures from UK government’s Abstract of Statistics, via Alistair McConnachie.).

The political repercussions from this loss of control over the money supply are vast. The graph provides a simple and direct explanation as to why government is constantly strapped for cash. If the same proportion of the money supply were under the aegis of the government now as in 1948 it would be able to invest on our behalf around half of the money put into circulation this year: £288.6 bn.

I am not suggesting we persuade our government to immediately create and spend this sort of sum. At minimum it would have a massively destabilising effect on the economy. It would also probably generate inflation; it would certainly generate a lot of talk about inflation. Along with most radical economists, I believe that the problem isn't insufficient money supply, but rather the opposite. So while one requirement is to readjust the balance between private and public money creation, the other is to tackle the overall quantity of money. But government has the power to affect the other side of the economy too. To deal with the inflation worries it would be perfectly feasible to constrain bank lending by an amount to match any newly created government issue. This would directly change only the shares of money, not the overall quantity. This is what governments are for, not standing on the sidelines waiting to be lobbied by interested parties.

The existence of Austin Mitchell’s motion stating that ‘credit has effectively been privatised’ and asking government ‘to redress the balance back to the people’ by creating money to fund public sector investment is a wonderful support for monetary reform. Perhaps the issue of PFI could be used to make this case in wider circles. The obvious conclusion to a consideration of the political consequences of the public-private deficit is that the government needs to show some real initiative and reclaim its right to produce the finance in our name to fund public services we all need to use.